What Happens If You Stop Paying Student Loans

Welcome, dear reader! Have you ever wondered what would happen if you stopped paying your student loans? The consequences can be serious and it’s important to understand your options. Whether you’re struggling to make payments or considering defaulting on your loans, it’s crucial to know the potential outcomes. Let’s dive into what happens when you stop paying your student loans and how you can navigate through this challenging situation.

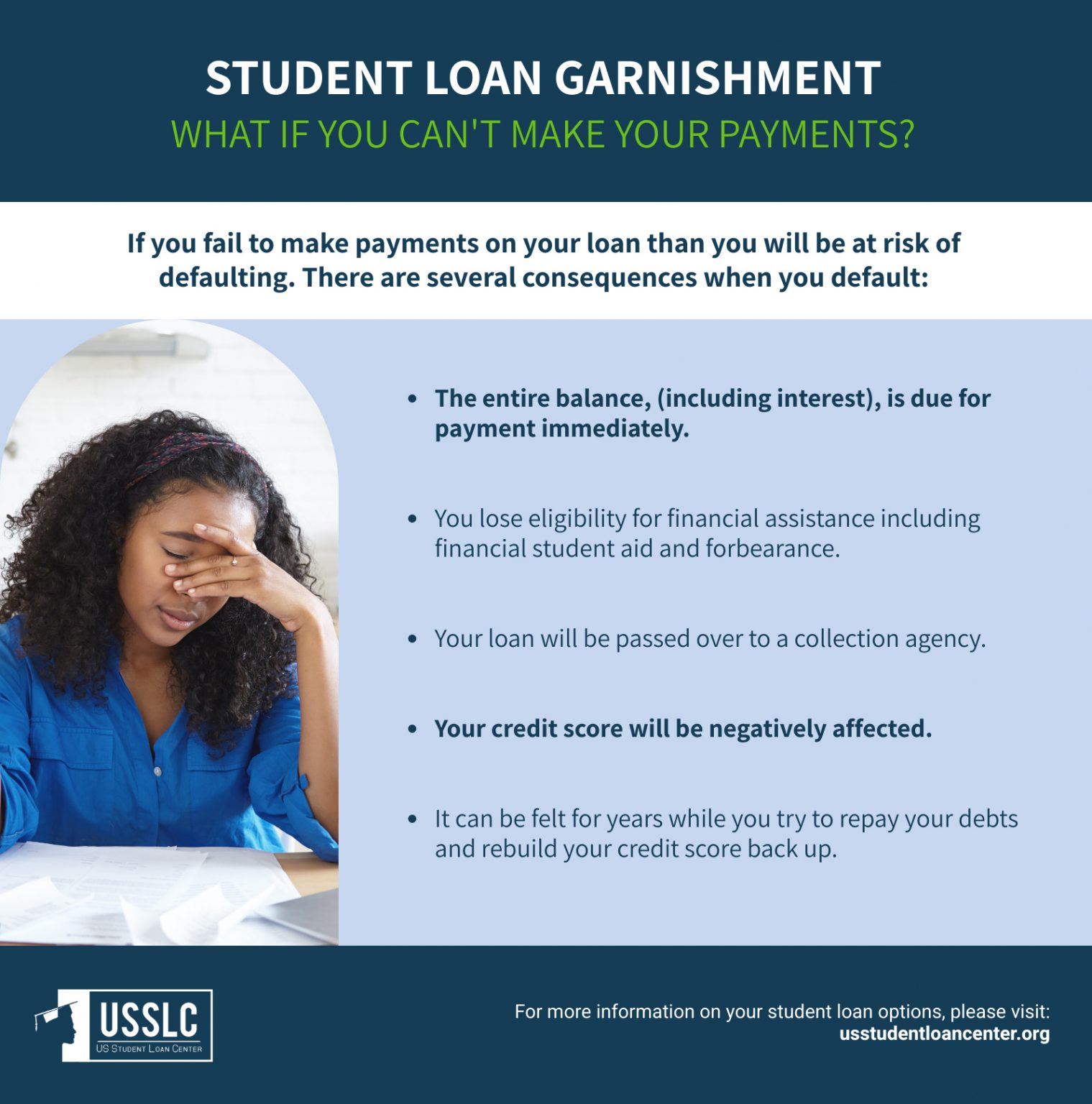

Consequences of Defaulting on Student Loans

Defaulting on student loans can have serious consequences that can negatively impact your financial future. When you stop making payments on your student loans, you are considered to be in default. This can lead to a range of consequences that can affect your credit score, financial stability, and overall well-being.

One of the immediate consequences of defaulting on student loans is damage to your credit score. When you miss payments on your loans, it can lower your credit score significantly. This can make it difficult to qualify for credit cards, car loans, and mortgages in the future. A lower credit score can also result in higher interest rates on loans, which can cost you more money in the long run.

Defaulting on student loans can also lead to wage garnishment. This means that your employer can withhold a portion of your paycheck to repay your debt. This can make it difficult to pay for everyday expenses and can further damage your financial stability.

In addition to wage garnishment, defaulting on student loans can also result in the offset of your tax refunds. The government can intercept your tax refunds to repay your student loan debt. This can be particularly frustrating if you were counting on that money for other expenses.

Another consequence of defaulting on student loans is the possibility of being sued by your lender. If you continue to ignore your loan payments, your lender may take legal action against you. This can result in additional legal fees and court costs, further adding to your financial burden.

Defaulting on student loans can also have long-term consequences. For example, if you default on federal student loans, you may be ineligible for future financial aid. This can make it difficult to further your education or pursue additional degrees in the future.

Furthermore, defaulting on student loans can also impact your ability to rent an apartment or secure a job. Many landlords and employers perform credit checks as part of the application process. If they see that you have defaulted on student loans, they may view you as a risky candidate.

Overall, defaulting on student loans can have far-reaching consequences that can impact your financial stability for years to come. It is important to take proactive steps to manage your student loan debt and avoid defaulting. This may include exploring repayment options, seeking assistance from a financial advisor, or contacting your lender to discuss alternative payment plans.

Impact on Credit Score

When you stop paying your student loans, it can have a significant impact on your credit score. Your credit score is a three-digit number that lenders use to determine your creditworthiness. Payment history makes up a large portion of your credit score, so when you miss student loan payments, it can cause your score to drop significantly. This can make it difficult for you to qualify for credit cards, auto loans, mortgages, and other types of loans in the future.

In addition to a lower credit score, missing student loan payments can also result in negative marks on your credit report. These negative marks can stay on your credit report for up to seven years, making it even harder for you to rebuild your credit. Potential landlords and employers may also check your credit report, so a poor credit score can have an impact beyond just borrowing money.

If you continue to miss payments, your student loans may go into default. When a loan is in default, the entire balance becomes due immediately, and the lender may take legal action to collect the debt. This can result in wage garnishment, where the lender takes money directly from your paycheck, or a lawsuit leading to a court judgment against you. These actions can further damage your credit score and make it even harder to recover financially.

Even if you are able to bring your student loans current after missing payments, the damage to your credit score may already be done. While late payments will still show on your credit report, bringing your loans current can help minimize the impact. It’s important to communicate with your lender if you are struggling to make payments, as they may be able to offer repayment plans or deferment options to help you avoid defaulting on your loans.

Wage Garnishment and Tax Refund Offsets

When you stop paying your student loans, one consequence you may face is wage garnishment. This means that a portion of your paycheck can be taken directly from your employer to repay the loan. The government can require your employer to withhold up to 15% of your disposable income, which can make it difficult for you to cover all of your expenses. Wage garnishment can also harm your credit score and make it harder for you to secure loans or credit in the future.

Another consequence of not paying your student loans is tax refund offsets. If you are entitled to receive a tax refund from the government, they can intercept that refund and use it to repay your outstanding student loan debt. This can come as a surprise to many people who were expecting a tax refund to help cover other expenses or make a big purchase. It’s important to note that the government can take your tax refund without warning if you have defaulted on your student loans, so it’s essential to stay informed about your loan status.

Wage garnishment and tax refund offsets can have a significant impact on your financial stability and future opportunities. It’s crucial to stay on top of your student loan payments and communicate with your loan servicer if you are experiencing financial hardship. There may be options available to help lower your monthly payments or temporarily suspend payments until you are in a better financial situation. Ignoring your student loan debt can lead to serious consequences, so it’s important to take action and address the issue as soon as possible.

Collection Agency Involvement

When you stop paying your student loans, the lender will typically not waste any time in trying to reach out to you to rectify the situation. However, if you continue to ignore their attempts at communication, they may eventually enlist the help of a collection agency to recover the debt. Collection agencies are third-party companies that specialize in pursuing unpaid debts on behalf of creditors.

Once a collection agency gets involved, they will begin contacting you through various means, such as phone calls, emails, and letters. They may also start reporting the delinquency to credit bureaus, which can have a negative impact on your credit score. These actions are meant to put pressure on you to start making payments towards your student loan debt.

Collection agencies are known for being persistent in their efforts to collect on debts. They may use aggressive tactics in their communication, such as threatening legal action or wage garnishment. It is important to keep in mind that while collection agencies can be intimidating, they are still bound by laws that govern debt collection practices. For example, they are not allowed to harass you or make false statements about the consequences of not paying your debt.

If you are being contacted by a collection agency regarding your student loans, it is important to respond to their communication. Ignoring them will not make the debt go away and will only make the situation worse. You may be able to work out a repayment plan with the collection agency or negotiate a settlement for less than the full amount owed. It is also possible to request validation of the debt to ensure that it is accurate and that you are indeed responsible for repaying it.

Ultimately, dealing with a collection agency can be a stressful and overwhelming experience. However, it is important to take action and address the situation promptly to avoid further consequences. By staying informed about your rights and options when it comes to dealing with collection agencies, you can work towards resolving your student loan debt in a way that is manageable for you.

Options for Managing Student Loan Debt

Defaulting on student loans can have serious consequences, both financial and legal. It is important to understand the potential effects of not making payments on your student loans.

When it comes to managing your student loan debt, there are several options available to help make repayment more manageable. One option is to explore income-driven repayment plans, which adjust your monthly payments based on your income and family size. These plans can help lower your monthly payments and make them more affordable. Another option is loan forgiveness programs, which forgive a portion of your student loans if you meet certain criteria, such as working in a public service job for a specified period of time.

Consolidating your student loans is another option to consider. This involves combining multiple federal student loans into one loan with a single monthly payment. Consolidation can simplify the repayment process and potentially lower your interest rate, making it easier to manage your debt. Refinancing is a similar option but involves obtaining a new loan from a private lender to pay off your existing student loans. Refinancing can help you secure a lower interest rate, potentially saving you money over the life of the loan.

If you are struggling to make your student loan payments, you may be eligible for deferment or forbearance. Deferment allows you to temporarily stop making payments on your federal student loans, typically if you are experiencing financial hardship or going back to school. Forbearance is another temporary option that allows you to pause or reduce your loan payments for a specific period of time. Both options can provide temporary relief from making payments, but interest may still accrue during this time.

Ultimately, the key to managing your student loan debt is to stay informed and explore all available options. It’s important to communicate with your loan servicer if you are experiencing difficulty making payments, as they may be able to offer assistance or alternative repayment plans. By proactively managing your student loan debt, you can avoid defaulting and minimize the financial and legal consequences that come with it.